600m TVL in 3 Months: Is Resolv the Better Ethena?

An exploration on the definition of good minted cash and Resolv’s design — the new, the risk, the goods and bads

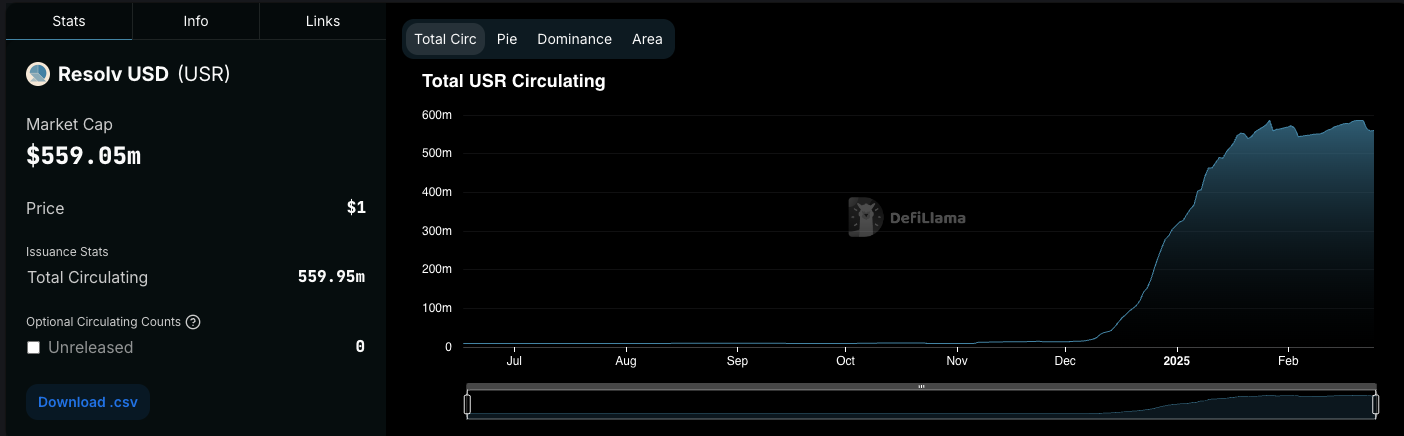

Within Decmber 2024, Resolv TVL grew from roughly 13m to north of 300m. Now with TVL approaching 700m, is Resolv the next star for synthetic dollar after ethena’s meteoric success? This blog is an exploration on the definition of good minted cash and Resolv’s design — the new, the risk, the goods and bads.

Disclaimer: I have no private round exposure to Resolv but do have yield exposure. This analysis is purely objective and based on public information only.

Define Money

The Basics: The Fed is NOT the only institution that increase the amount of money floating — anyone can increase the money supply by facilitating debt. If A lend $100 to B, all of a sudden that $100 is on both parties’ balance sheet: A’s assets and B’s liability. However, since B might default on the debt, A’s assets, the account receivable, is not guaranteed. Thus, A’s account receivable is an floating-value asset, NOT STABLE-VALUE CASH.

When we talk about stablecoins, we are talking about stable-value cash. So what gives one ‘the right to mint cash’ if you are not the Fed? Here’s my definition of a good stable-value minted cash:

over-collateralized, backed by relatively stable value, highly liquid assets

near instant conversion to widely-accepted stable money (eg. USD, USDC, USDT, DAI) without damaging over-collateralization

controlled counter-party risk (eg. solvency, custodian)

Crush Course on Resolv’s Design

(these are promises made by the Protocol. In the next section we will evaluate whether these promises are realistic.)

USRis the non-yielding stablecoin, pegged to dollar, principle-guaranteedstUSRis staked version ofUSR, yield-bearing, pegged to dollar, principle-guaranteed, instant unstakingRLPis the riskier, higher yielding assets, NOT pegged to dollar, without principle-guarantee and with redemption delay (1 day) or redemption pause (when total backings <110% of USR &stUSRfloating). Its backings act as buffer capital whenUSR / stUSRbacking becomes insufficient.wstUSR is the non-rebasing version of

stUSRfor defi composability purpose$RESOLVis the pre-launch native-token, currently serves as an incentive for people to hold unstaked USR, in order to amplify yield for those who stakeUSR

When user deposit liquid stables (eg. USDC, USDT, DAI, USDe), Resolv protocol opens a delta-neutral position which consists a long LST and a short perp. This future basis mechanism is the same as ethena — the current leading synthetic dollar protocol.

As of March 6th 2025, stUSR’s 7-day APY is 5.9% (530M TVL) and RLP’s 7-day APY is 11.1% (105M TVL). The TVL ratio of RLP:USR is ~20%, which provides decent buffer for the backings of USR holders. With Ethena’s sUSDe returning 5%, Sky’s sUSDS returning 6.5%, short-term t-bill returning 4.2%, and AAVE USDC lending returning 3.5%, Resolv’s USR and RLP yield looks decent.

The New

Trenches as Buffer: RLP is riskier-tier, higher yielding buffer capital. Instead of using the centralized-planned reserve capital (ie. how Ethena does it) to provide the protocol an extra layer against insolvency, Resolv let THE MARKET decide on the amount of reserve and price of buffer. RLP backing is supposed to consist of 10-30% of TVL but get 70-80% of the yield generated by all delta-neutal backings. In return, if the protocol’s backing ever becomes insufficient to make whole of all USR (stablecoin, safe-tier), the backings of RLP are used to make up for the loss.

Let’s walk through an example. Alice uses 100 USDC to mint RLP. Since RLP is freely traded, floating value token, the amount of RLP minted is determined by the current traded price of RLP. Say RLP is traded at $1.1, then Alice mints 100/1.1=90.9 RLP, representing 100 USDC worth of delta-neutral backings. When backings value is sufficient for both RLP and USR, RLP price will continue to be 1.1 in an efficient market. Let’s assume the RLP:USR ratio is 20%.

(the math code of the next two paragraphs can be found here)

If the backing returns 9% APY in total, 70% of total returns go to RLP holders who provide only 20% of the total capital. The rest 30% go to stUSR holders, who along with USR holders, provide 80% of capital. This net to (0.090.7/0.2=) 31.5% APY for RLP holders and (0.090.3/0.4) 6.75% APY for stUSR holders, assuming half of floating USR is staked. This sounds quite attractive!

However, currently with approximately half of floating USR staked, the return on total backings is only ((105m0.011 + 265m0.059) / 633m =) 2.65%.RLP tier is getting only 35% of all yields while providing 16% of capital — much less than the 70% yield on 20% capital as mentioned in the doc. Right now Resolv can’t afford to split yield 70/30 because the 2.65% overall yield would drags the safe tier yield to 1.9%, which is a non-starter in the competitive landscape of the current market.

In extreme distressed situations such as centralized exchange hacked and Resolv protocols lost 10% of its backing value, then USR holders can still be made whole but RLP holders lost half of their backings. RLP redemption is also paused because the protocol only allows redemption if the total collateral is >110% of total USR / stUSR floating. RLP’s value will approximately halve in secondary market, since it now only have half of the backings + currently being illiquid for redemption. Even if redemption is not paused, RLP holder can only redeem 50 cents on a dollar.

If someone mint RLP during distressed times, the RLP will be cheaper and thus leading to even higher yield — an extra incentive for the market to provide buffer capital during distressed times. I do think let THE MARKET decides on buffer amount and price is structurally better than the centralized planned reserve fund used by Ethena. Since reserve fund is retained from protocol earnings, it needs time to build up after distressed period — the time you might not have if two large-scale withdraw / hacks happen together.

The examples below from Resolv’s doc best explain profit / loss distribution between RLP, USR, and stUSR holders

Borrow ETH against LST: Since not all derivative exchanges accept ETH LSTs as collateral to open short positions, the protocol needs to get ETH while maintaining the ETH LSTs position. Using ETH instead of ETH LSTs also controls LST depeg risk that might lead to liquidation at derivative exchanges.

Holding ETH LSTs and borrow ETH to open the short only makes economic sense if the interest paid on AAVE is less than the LST yield, and this interest can be lowered by borrowing less ETH and use leverage at the derivative exchange. The borrowing cost of ETH is around 2.65-3% while supplying stETH yields merely 0.1%. With 3.3% stETH yield, this trade is profitable by 50-80 basis points.

In contrast to Resolv’s 50% ETH LSTs cap and its proactive approach to earn ETH LSTs yield + future basis yield, Ethena only has 4% of total backing assets in ETH LSTs despite having another 19% of backings in ETH. This allocation is for prioritizing liquidity and minimize counterparty risk. Is the 50-80 additional basis points worth the potential iliquidity and LSTs / AAVE counterparty risk? I think it has a much lower sharpe ratio than some other yield sources, which we will get to later.

This downsizing of ETH LSTs is also due to Ethena’s increasing allocation to liquid stables — namely USDC on CEX earning rebate T-Bill yield. With roughly 3.5B out of 6B TVL staked and returning 9%, Ethena is returning 5.25% on it’s underlying — which is only 100 basis points higher than the current T-Bill rate. That’s not super high as a future basis protocol when centralized exchanges’ premium APY ranges from 6-15%.

So for both protocols, the amplification of yield really matters! You have to figure out a way to incentive half of your holders to not stake in order to be the cool protocol that says you have an attractive (ie. 6-12%) future basis yield. Both protocols use their native token as incentive to keep half of their stablecoin holders from staking, which seems to have a honeymoon effect at the beginning but struggle to sustain the peak level yield and liquidity. If you are a defi veteran from summer 2020, you know this play and I will say no more.

Use margin to open short: While Ethena wants to minimize leverage, Resolv uses margin ratio as low as 20% to open shorts. This means if the market pumps by 20% and Resolv hasn’t put up more collateral, their positions might get liquidated at centralized derivative exchanges.

With 99.9% probability, the system can put up sufficient collateral by borrowing ETH or selling ETH LSTs for ETH. However, a good synthetic stablecoin protocol is all about showing your customers that you can survive the 0.01% probability market. Under extreme volatile market, ETH LST depeg risk and borrowing cost both might increase to cause stress to the system.

I predict there would be a synthetic stablecoin that lose peg this cycle because the overall market sentiment is too bullish. Here’s how it might play out: super bullish market. majors go up 15% in one day. funding rates go up to 40% (we’ve seen this many times in 2020/21). more people want to sell their synthetic stables to join the bull saga. protocols can’t close those delta-neutral positions when funding rate is that high, which leads to 1/ withdraw pause; or 2/ close at loss → depeg.

I also want to point out here that the fear of prolonged negative funding rate (perp short pay perp long) leading to depeg DOESN’T MAKE ANY SENSE. When funding rate is negative, you can close your position at gain. So synthetic stables protocols should fear extreme bull much more than extreme bear. I do think fearing bull is a much better position than fearing bear, because at least the protocol can say “sorry you can’t withdraw at this moment, but your stablecoin is earning 40% future basis yield.” This is definitely a step forward for this space. Before future basis stables, all CDP/algorithmic stables fear bear.

The Risk

RLP’s return not being sufficient to justify its risk. Ethena uses its reserve fund mostly to protect against 1/ loss of unrealized gains at centralized exchanges; 2/ loss due to not open / close positions promptly. 1/ significantly overweights 2/. For example, after the 1.4B bybit hack in Feburary 2025, Ethena claimed that their customers could still be made whole even if they lost all 40m of unrealized gain in the event of bybit insolvency. Ethena also claims to use reserve as a buffer during prolonged negative funding rate period. However, as I mentioned above, since the protocol can close position at gain when funding rate is negative, loss only occurs during negative funding rate IF positions aren’t closed promptly.

According to Julio Moreno’s analysis, Ethena needs to put 20% of yield into reserve fund in order to maintain reserve fund at a healthy level — a 1.15% buffer. 20% is A LOT. It’s also not capital efficient compare to how Resolv uses 49% of yield to attract a 15% capital buffer. By the end of the day, our on-chain world is never short of risk-tolerant capital that want the higher return, so let this market do its magic is better than centralized planning.

Based on the frequency of volatile market and Ethena’s need for reserve fund in the past 15 months, it’s fair to say that buffer capital has a high probability to take hit, and the mere 11% APY for RLP is definitely not enough to convince me to put money in it. Right now, RLP provides 16% of capital while gaining 49% of yield. Given the risk, RLP should gain more asymmetrical returns — perhaps 70% yield for 15% of capital. You can play around with the simulation I wrote.

However, the bottleneck comes down to not being able to get the overall yield up. The protocol is facing a peculiar situation: 1/ don’t want lower yield for stUSR to stay competitive in yield-bearing stables game; 2/ want returns for RLP be sufficient to attract 10%+ buffer capital for USR; 3/ get the overall yield up without engaging in risky lever that scares RLP investors

But success comes from thriving amid constraints.

Buffer capital scalability. For the protocol to scale another one or two orders of magnitude, there needs more sophisticated liquidity to come in, compete, and price the risk and reward. Since Resolv seems to be the only sizable shop in town exploring this buffer capital design, the market buffer capital market is FAR FROM free and efficient yet — which means HIGH BETA for those who participate in the market right now. You can think of the current situation as — Michael Milken just started to explore high yield bonds; Dan Valentine wrote Jensen his first check.

The Summary

The Pros

RLP and USR holders aren’t each others’ counterparties. Your EV is the integral of your projected probability of return distribution, thus both tiers can be perceived as fair value and high EV because people have different projected probability of return distribution.

Let market decides the amount and price of the buffer is better than centralized planning

Incentive (yield) rises when buffer capital runs low to prevent prolonged distressed market situation from depleting the buffer capital

10% guaranteed buffer for USR because of the 110% collateral requirement for RLP to start redemption

The Cons

Overall backing return (2.65%) is too low. “My competitiveness relies on keeping half of the stable holders away from staking” is not a sustainable position to be in.

Use margin to open short introduces more risk surface for only 50 bps of extra returns

Borrow ETH against WSTETH exposes the protocol to borrowing cost on AAVE

49% yield allocated to RLP is likely insufficient to produce a positive EV result for RLP holders

Reference:

https://dune.com/saul/resolv-labs-dashboard

https://x.com/jjcmoreno/status/1780336592403448045

https://substack.com/home/post/p-146169059